#3 - Finolex Industries - A major player in the Plastic pipes industry

Finolex Industries is India’s largest manufacturer of PVC pipes & fittings and a leading producer of PVC resin. The company is the only large vertically integrated player in the domestic market which produces its entire requirement of PVC resin, the major raw material used in manufacturing PVC Pipes & Fittings.

Industry Structure and Tailwinds for growth of Plastic Pipes -

Below is the market share of Major players as on 2019. The market share for major players hasn't changed much in FY 2021. The major listed players are Supreme Industries(11%) , Finolex Industries (9%) , Jain Irrigation (8%), Astral (7%) and Prince Pipes(5%).

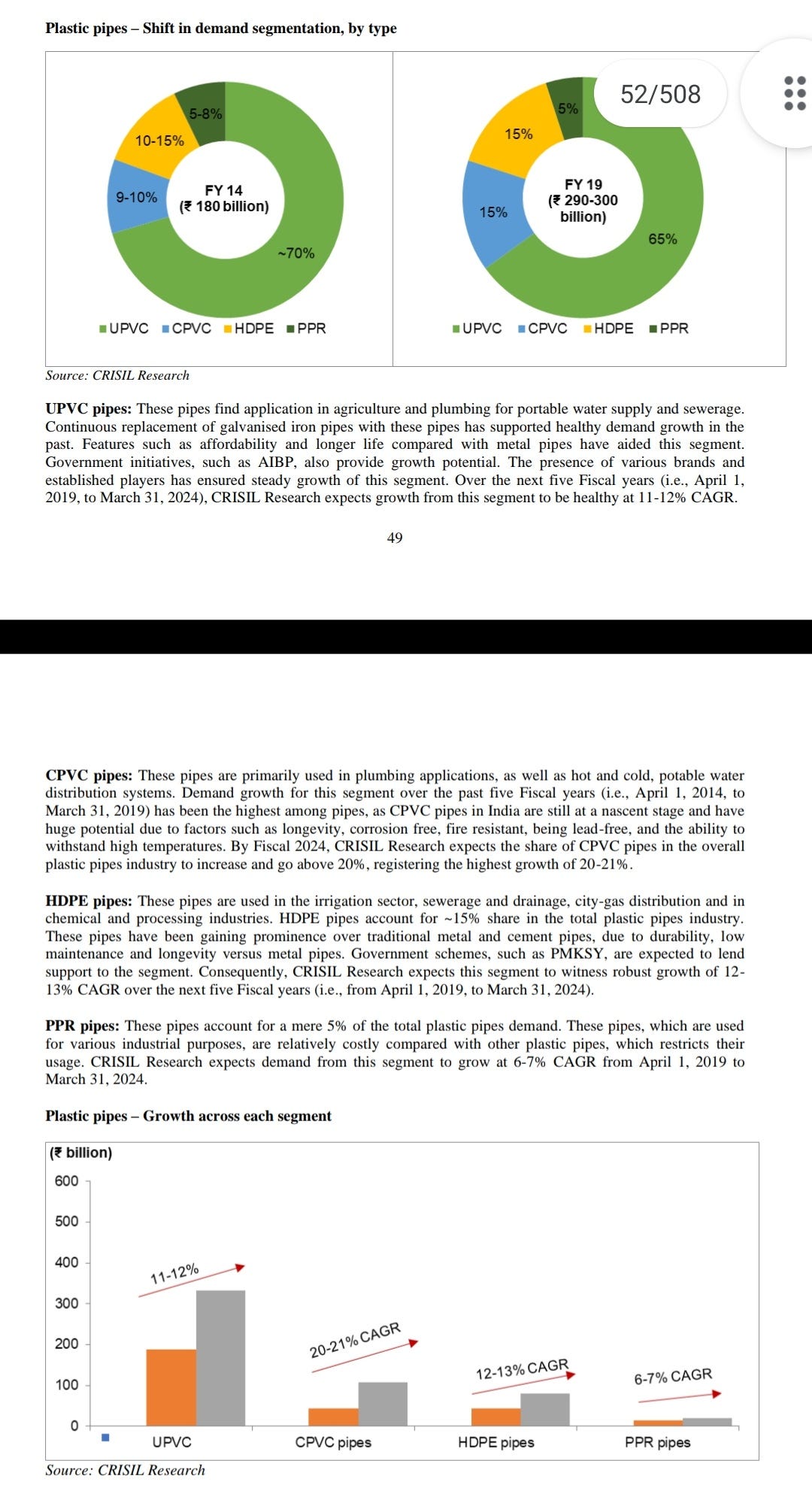

Plastic pipes are more durable, cheaper and do not rust as compared to Metal GI pipes. This has resulted in mass adoption of PVC pipes used in agriculture and real estate and they have replace Metal GI pipes. Below is the overview of Indian Plastic pipes industry and why they are better than metal GI pipes for both plumbing and agricultural purposes.

Plastic pipes are used in 3 areas majorly - Agriculture, WSS (Water Supply and Sanitation)and plumbing(mainly used in real estate) and Sewerage.

Below are the end uses of different types of pipes and the industry they cater to.

Below are the competitors of Finolex Industries -

Astral Limited - One of the larger players in plumbing/SWR pipes used in real estate. Piping division contributes 77% of topline.

Units sold in FY 21 - 1,36,590 metric tonnes (P.Y - 1,32,200 metric tonnes)

Total Capacity - 2,57,946 metric tonnes.

Supreme Industries - 65 % revenue comes from plastic pipes and fittings. Supreme Industries with Finolex Industries are the biggest players in PVC pipes by market size and the two have a bigger presence in PVC used in agriculture.

Units sold in FY 21 - 2,94,357 (FY 20 - 3,00,722) metric tonnes.

Prince Pipes - Units sold 1,38,289 metric tonnes (FY 20 - 1,32,816 metric tonnes).

Installed Capacity - 2,50,000 metric tonnes.

Prince pipes is one of the larger players in plumbing/SWR pipes used in real estate.

Industry tailwinds - PVC pipes prices are dependent on crude oil prices and crude is a major raw material for all this players. PVC prices have increased from 600 USD/MT to around 1700 USD/MT. Below is the PVC price chart from January 2018 to March 2021.

Finolex Industries - Finolex Industries is a major player in plastic pipes Industry especially in the agricultural vertical.

PVC pipes sold in FY 21 - 2,12,060 metric tonnes (P.Y - 2,54,958 metric tonnes)

Total Capacity - 3,70,000 metric tonnes.

PVC resin sold - 2,36,086 metric tonnes (P.Y. - 239,188 metric tonnes)

Key Factors for Finolex Industries -

Backward Integration - Finolex Industries are backward integrated and they manufacture PVC resin which is a key component for PVC pipes. Entire demand for PVC pipes and fittings is absorbed by in-house manufacture of PVC resin and the company sells the balance to other parties.

Cash and Carry Model - The company has a cash and carry model which means their debtor days are at 7. This means the company is more efficient in passing off the price fluctuations more efficiently than other players. This also means robust collection as evidenced by CFO/EBITDA ratio which stands at an impressive 87%.

Assets - The company is net debt free and in an industry where other competitors(Jain Irrigation/ Kisan Moulding) are struggling with debt issues this is a big positive. The company holds land of 70 acres which should on conservative basis should be valued at 400 crores. The company also holds 14.53% share in Finolex Cables which is valued as on date at around 1139 crores. This gives assets on book at 1500 crores or 14% of the market capitalization.

Reasonable Valuations - Finolex Industries is valued at 14.6x PE (12.5x if you exclude other assets) which is extraordinarily low compared to Peers -

Astral Limited - 95.4 PE

Supreme Industries - 27.5 PE

Prince Pipes - 34.7 PE

Possible Headwinds for Finolex Industries -

Rapid growth of competitors - The growth of Astral Limited and Prince Pipes due to heavy advertisement has seen them gain market share and grow rapidly compared to Finolex Industries in the last few years, if the trend were to continue it could result in Finolex Industries losing substantial market share in the long run.

Monsoon - Finolex industries sells 70% of PVC pipes in the agricultural space and 30% in the construction space. Incase of a poor monsoon, the company will be affected more adversely than it’s competitors.

PVC price - Substantial drop in PVC pipes can result in a lot of profits being wiped off which were recorded in the current year, this is an industry wide phenomena and will affect the entire industry.

Conclusion - In Finolex Industries, I see a company which is reasonably valued in an industry which is expected to grow at 9%-10% in the agricultural space and at 14-15% in the non-agricultural/ construction space in addition to gaining market share from unorganized players. The possibility of failure of Jain Irrigation, a major player cannot be ruled out which may result in capturing of market share, however it is more likely the company may be acquired via NCLT. A dividend yield of over 2 percent is an added positive.

Disclosure - Invested from Lower Levels.

Market Cap of the company - Rs. 10793.2 crores.

If there is a company in the small and midcap space 500-30000 crores you would like me to write me about, please drop a comment.

Here are the links to other companies I have covered -

Godrej Agrovet - An all-inclusive bet on Indian Agriculture

https://cashcows.substack.com/p/godrej-agrovet-the-best-way-to-play

SastaSundar Ventures - A small cap E-pharmacy company with high potential for growth - https://cashcows.substack.com/p/sastasundar-ventures-underpriced

Here is an alternate valuation methodology I use -https://cashcows.substack.com/p/an-alternate-valuation-model-consistent

Good analysis. Is there any premiumization angle here? I remember vaguely from my past analysis that there was a distinct mass vs premium market and players like Ashirvad played more at the premium end (could be wrong). Hence the question.

Separately, have you looked at ELGI equipments? Would like to read your analysis on that - especially the headwinds / risks you see to the market thesis and the reasons for the premium valuation.

Great analysis , can you please review Sequent scientific .